The recent Spirent article rightly highlights the potential of 5G-Advanced (5G-A) and the role of the 5G Core in enabling monetization. However, 5G-A should be seen primarily as a future-oriented evolution rather than a current monetization engine, but why?

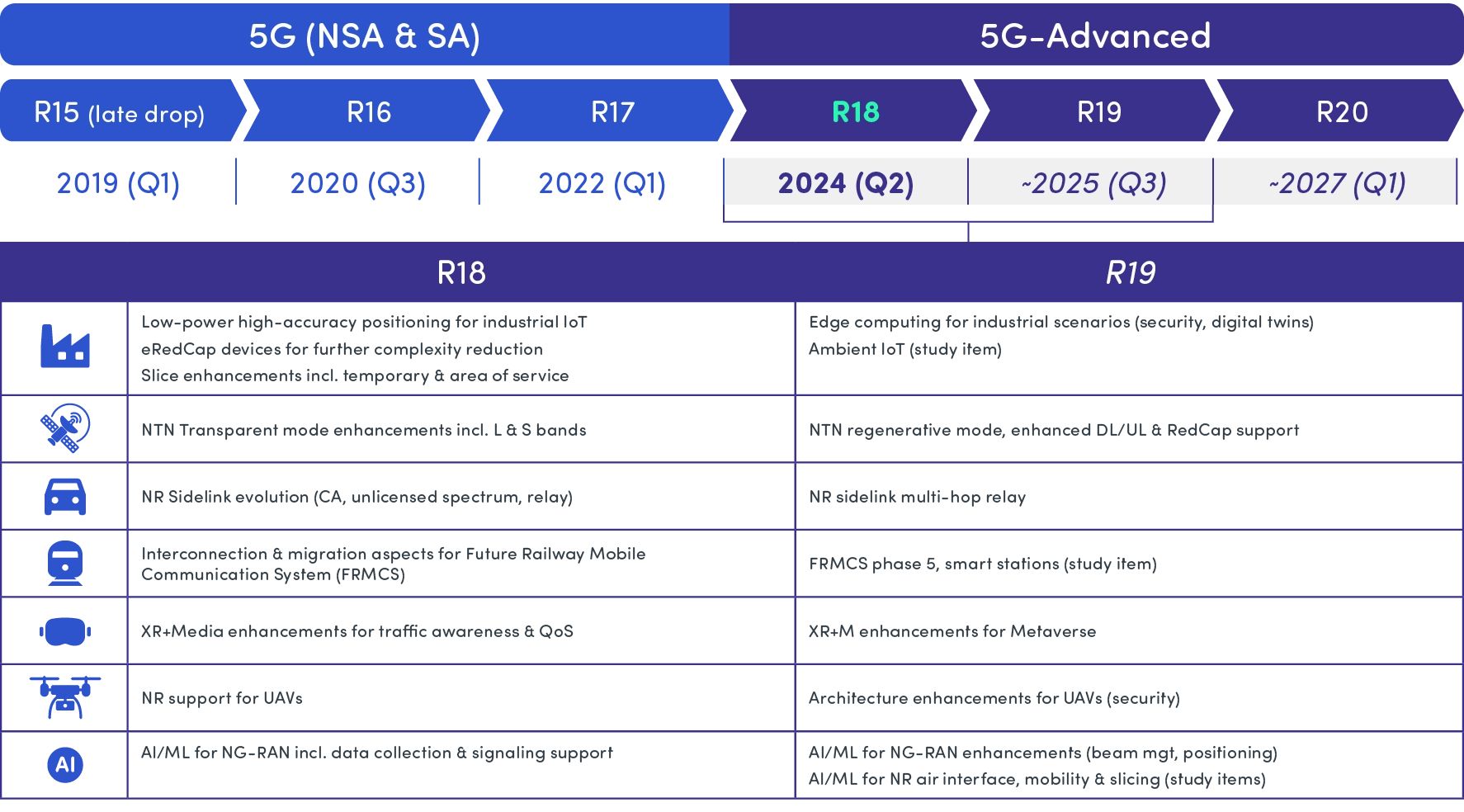

- Release 18 standards are just being finalized. Most mobile operators are still expanding 5G standalone (SA) and seeking ROI from earlier investments in mid-band spectrum.

- Advanced features like network slicing, exposure platforms, and XR support seem promising, but commercial traction is limited. These will scale as the ecosystem—devices, applications, and regulations—mature in 3–5 years.

- 5G-A adoption will #not be uniform worldwide, as per GSMA. Less than 20% of global operators have launched 5G SA commercially, a prerequisite for 5G-A features.

- As per Ericsson, while 80% of CSPs now offer FWA, fewer than 10% are actively testing 5G-A capabilities.

Operators should not expect short-term revenue lifts from 5G-A. Instead, it should be viewed as a strategic roadmap for the second half of this decade, with timelines and business models varying widely across regions.

The real challenge is ensuring 5G-A doesn’t repeat the “hype vs. reality” gap seen with initial 5G